By Michael Bray

Professor of Practice (Integrated Reporting) – Deakin University, director of the International Integrated Reporting Council, former partner – KPMG Australia.

Integrated reporting assurance is emerging: its place in the pathway to the audit of the future is becoming clearer.

Early assurance on integrated reports has been achieved on an incremental basis, with numerous instances of limited assurance on selected metrics, such as under GRI standards, in integrated reports. In South Africa, ‘combined assurance’ has proven a popular assurance model.

Assurance in accordance with the International <IR> Framework is now emerging with five known instances of integrated reporting assurance ‘in accordance with’ the International <IR> Framework (to be distinguished from assurance on selected GRI metrics in integrated reports) to date. Example 10 in the International Auditing and Assurance Standards Board’s proposed guidance on Extended External Reporting Assurance, an integrated reporting assurance example, should be a propellant of more integrated reporting assurance and a guardian of its quality.

Unique challenges and opportunities of integrated reporting assurance flow directly from the distinctive contribution of integrated reporting. This underscores the importance of guidance for assurance practitioners on evaluation of the narrative describing The Business and resulting self-determined, business-critical metrics (mainly regarding intellectual capital) in an integrated report.

This will involve judgement (by the assurance practitioner) on judgement (by those charged with governance on reporting of The Business) on judgement (business judgements by executive management on The Business – its strategy, business model and approach to risk and opportunity management) – business insight. It will also involve business measurement judgement by management and the assurance practitioner on which self-determined metrics (some will not be in financial and sustainability reporting standards e.g. intellectual capital metrics) best tell the story of the ability of The Business to create value in the short, medium and long term – performance insight.

The Value of Integrated Reporting Assurance

Thinking about the value of assurance for stakeholders, and using the concept of discounted cash flows (DCF) as a proxy for broader stakeholder thinking and decision-making, an example can be constructed using the impact of social licences being subject to financial sanctions, restricted or in a worst case removed as an example. Such licence changes can have catastrophic impacts which can and should have an impact on investor and analyst decision-making. Other stakeholders can use this thinking in their own engagement and decision-making activities. An assured integrated report will contain credible ‘raw materials’ to support such decisions.

Take for example a major environmental incident or loss of a key piece of intellectual property. The removal of a social licence to operate or key piece of intellectual property can result in the elimination or severe reduction of cash flows at least in the long-term. An investor or analyst, or other stakeholder using DCF thinking as a proxy, may reduce their short- or medium-term projections of cash flows or make a discount rate adjustment, if a financial sanction or licence restriction is imposed. Terminal value (long-term) is often thought to be upwards of 40% of net present value and may be removed from a stakeholder’s financial model or thinking for a projected loss of licence or key piece of intellectual property.

The value of integrated reporting assurance – paraphrased, ‘Dear stakeholder, the real strategy and business model is disclosed in the integrated report’ – will be valued by investors and other stakeholders for enhancing their decision-making and will be in the public interest – a basis for instilling stakeholder confidence and trust.

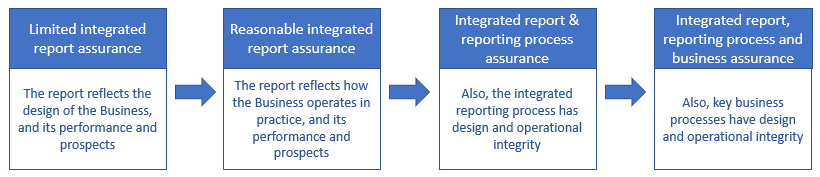

The Roadmap to the ‘Audit of the Future’

The pathway from integrated report assurance to integrated reporting assurance to integrated assurance can be seen as a roadmap to the ‘audit of the future’:

The ‘audit of the future’ is critical to the public interest, the future of the accounting profession and the careers of accountants. At a macro level, it can be an important contribution to business productivity, capital markets, society and international competitiveness. The pathway to integrated assurance is underway with the emergence of instances of limited assurance of integrated reports in accordance with the International <IR> Framework.